Market trend

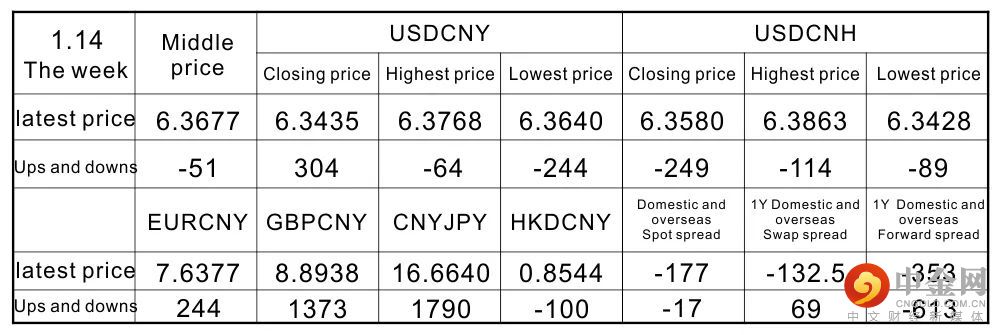

The central parity rate of the US dollar against the RMB was reported at 6.3677 on Friday (January14),and the central parity rate of the RMB was lowered by 51 pips compared with last week (January 317) . 304pips and down 249pips . As of 5:00 pm on Friday , the spot and 1 -year forward spreads of domestic and foreign RMB were 55pips and -87pips respectively . EUR/RMB was reported at 7.2591 , GBP/RMB at 8.6880 , RMB/JPY at 17.9242 , HKD/RMB at 0.8178 , an appreciation of 224pips , an appreciation of 341pips , an appreciation of 348pips and a depreciation of last week respectively2147pips .

In terms of funds, the inter-bank market liquidity tightened on Thursday, most of the main repo rates rose, and the overnight supply was slightly insufficient, and the transaction price increased all the way up . Although there are still a few days before the tax payment, but in January , it is still faced with the superimposed effects of routine payment and the peak of cash withdrawal before the holiday. We will pay attention to when the amount of reverse repurchase in the open market will increase. The continuation of MLF next Monday is still the focus of the market, especially whether the interest rate will be lowered is still attracting much attention, which will directly affect the expected direction of the next policy. Li Keqiang presided over an executive meeting of the State Council a few days ago, and made it clear that stable growth should be given a more prominent position, insisted on not engaging in “flooding”, and targeted expansion of final consumption and effective investment ; The funds for special government bonds will be allocated to specific projects; the special bonds issued this year will be issued promptly, and efforts will be made to create more physical workloads in the first quarter. The liquidity gap in January may reach 2.6 trillion yuan (not considering the maturity of MLF and reverse repurchase), which is at a relatively high level. The central bank's operation strength is the most critical variable. It is likely to smooth out fluctuations through OMO+MLF , but it is difficult to realize significantly loose. At present, some investors are starting to bet on the central bank to cut interest rates in January , but we do not think the probability is high. Considering that the current level of increased leverage in the bond market is still on the high side, the impact of changes in liquidity is expected to be magnified accordingly. We need to be alert to the risk of rising interest rates after the market's overly optimistic expectations have failed. Since January 1 , the central bank has implemented the two direct tools of the Inclusive Small and Micro Enterprise Loan Extension Support Tool and the Inclusive Small and Micro Enterprise Credit Loan Support Plan. The first is to convert the Inclusive Small and Micro Enterprise Loan Extension Support Tool into an Inclusive Small and Micro Loan Support Tool. The second is from 2022Since 2009, the Inclusive Small and Micro Enterprise Credit Loan Support Program has been incorporated into the re-loan management for agriculture, small and micro enterprises. Create two monetary policy tools that directly reach the real economy, support financial institutions in deferring the repayment of principal and interest on loans to small and micro enterprises that encounter temporary difficulties, and encourage financial institutions to increase credit loans to small and micro enterprises. The central bank released the 2022 work outlook, and it is necessary to increase financial support in key areas; implement the inclusive small and micro loan support tools and the inclusive small and micro enterprise credit loan support plan to continue the conversion work; continue to improve the financial support technology innovation system; correct understanding And grasp the carbon peak and carbon neutrality, and strengthen the overall coordination and orderly progress of green finance work.

Interpretation of key data and events

1. The three factors of vegetables, meat and non-food consumer goods drove the December CPI to fall back to the “1%” range year - on -year , reaching 1.5% (the previous value was 2.3% ), the direction of decline was in line with expectations, and the speed of decline was slightly faster than expected (our expectation). 1.8% ) . Of the 0.9pct that fell from the previous month , the three major factors dragged down 0.4pct , 0.1pct and 0.3pct respectively .

Interpretation:

The fall in vegetable prices is in line with our short-term judgment of the impact of rising vegetable prices in the previous period. The impact of the sharp rise in vegetable prices caused by the low temperature and rainy seasons in summer and autumn and the reduction in vegetable production may be short-lived. After December 2021 , vegetable prices in southern China may fall after the market . . In December 2021 , the CPI for fresh vegetables fell by 8.3% month-on-month , and dropped sharply from 30.6% year-on-year to 10.6% . The fall in the price of live pigs is in line with our previous rebound and non-reversal, the turning point of the pig cycle or the judgment in Q2 . The volatility of this round of pig cycles is larger than that in the past, mainly because of the impact of African swine fever in the early stage, the profits are huge at the high point, and it is difficult for farmers to exit when the losses are shallow. The peak of the inventory in July does not mean the peak of the production capacity, the proportion of binary pigs is increasing, and the population efficiency is optimized . Therefore , the rebound of live pig and pork prices in October-November last year was not a reversal, but due to the rapid price drop period in 21Q2 , the large pigs were thrown into the slaughter, and the demand for slaughtered pork was boosted by festivals and cured bacon. The production capacity may still be high. In December and January this year , large and small farmers still have the motivation to concentrate on slaughtering before the Spring Festival. In December , the price of live pigs did not rise but fell. The CPI pork price rose slightly by 0.4% . 36.7% . After the Spring Festival, the price of pigs may still fall, and then it may be an upward turning point in this round of pig cycles. The CPI of non-food consumer goods began to fall year-on-year, which is in line with our judgment that the PPI has always been in the CPI transmission, and the transmission time lag is 2-3 months. In November , the PPI fell year-on- year, while the CPI rose sharply. There is a view in the market that the PPI has begun to transmit to the CPI . In fact, the transmission of the PPI production means to the living materials and the PPI to the CPI non-food consumption has been going on for about 2-3 months. time lag, some categories have a time lag of 3-6 months. In December , the CPI for transportation and residential fuel, transportation, and medicine all dropped year-on-year. The performance of service prices was mixed, and the overall service CPI was unchanged at 1.5% year-on-year and the previous month . Affected by the disturbance of the epidemic and the slow recovery of income, the prices of hotels, rents and services were weak, but the prices of housekeeping services continued to increase year-on-year. The effect of the domestic policy of ensuring supply and stabilizing prices continued to show, and the Fed tightened in advance to restrain international bulk prices. In December , the PPI further fell to 10.3% year-on-year (previous value 12.9% , our expectation was 11% ), the first drop after 18 months from the previous month ( -1.2% ). Among the 2.6pct PPI that fell more than last month, tail- raising factors and new price increases each contributed half; in terms of industries, petrochemicals, coal, ferrous non-ferrous metals, and non-metallic minerals dragged down 2.8pct , while electricity marketization The reform continued, and the rise in electricity prices continued to drive 0.1pct positively ; in terms of major categories, the mining, raw materials and processing industries in the PPI production materials all fell significantly year-on-year, the food and clothing in the living materials fell, the general daily necessities were flat year-on-year, and durable goods were year-on-year. Still a slight increase, due to the influence of conduction time lag. Looking ahead, under the constraints of a high base, supply and stable prices, and the Fed's early tightening of bulk prices at home and abroad, the PPI may continue to fall year-on-year, and the pace and intensity of the stabilizing growth policy will determine the speed of the PPI fall. Since late November , the price of thread futures has bottomed out and rebounded, taking into account the expectation for the steady growth of infrastructure construction. It is still necessary to observe whether the infrastructure construction can accelerate as scheduled based on high-frequency data. Affected by the epidemic, the price adjustment of vegetables and meat, and the fall in cost, we believe that the CPI may remain in the “1%” range for several months, and the future upward pace still depends on the strength of easing fiscal and stabilizing credit. Although this year's “ in-place Chinese New Year ” policy is more flexible than last year, there are frequent epidemics in Xi'an, Henan, Tianjin and other places, and the introduction of Omicron , psychological factors may have a greater impact on choosing “ in-place Chinese New Year ” , and service prices may Still under pressure; high-frequency data in early January showed that fresh vegetable and pork prices continued to fall, despite the dislocation of the Spring Festival, under the high base and weak new growth, January CPI may fall further year- on - year, coupled with the fall in PPI and the pig cycle The inflection point may still have to wait until Q2 , and we expect that the year-on-year CPI may still hover in the “1%” range for several months.

2. In December 2021 , exports (in US dollars, the same below) increased by 20.9% year-on- year ( 22.0% year-on-year in November ), and imports increased by 19.5% year-on- year ( 31.7% year-on-year in November ), exports were higher than market expectations, and imports were lower than market expectations (Bloomberg consensus estimates were 20.0% and 27.8% , respectively ). The trade surplus was $ 94.5 billion ($ 71.7 billion in November ), a record high. In 2021 , exports will increase by 29.9% year-on- year, and imports will increase by 30.1% year-on-year . External demand is still strong, and domestic demand continues to show signs of stabilization driven by the manufacturing sector. The changes in the export structure in December more reflected the slight improvement in the global supply chain. We expect that the impact of the Omicron virus on the global supply chain may be less than that of the Delta virus, and China's exports in 2022 will still be good.

Interpretation: External demand is still strong. The number of confirmed cases of COVID -19 worldwide in December was 25.43 million, a sharp increase from 15.5 million in November . However, the epidemic prevention measures were generally not tightened significantly. The negative impact on the economy was less than the impact of previous epidemics. The global comprehensive PMI fell slightly by 0.5ppt compared with November . to 54.3% . Exports in December also continued to maintain a high growth rate under a high base. From a regional perspective, demand in the United States is still relatively strong, with a two-year compound growth rate of 28% , higher than the 24% in November , and exceeding the usual seasonality; the two-year compound growth rate of the EU and ASEAN has both declined. From the perspective of products, the two-year compound growth rate of high-tech product exports was 25% , higher than 18% in November . Among them, the two-year compound growth rate of mobile phone exports was 25% , higher than 2% in November , while labor-intensive products The two-year compound growth rate was 14% , down from 20% in November . Domestic demand, led by the manufacturing sector, continued to show signs of stabilization. Although the year-on-year growth rate of imports was lower than expected, the two-year compound growth rate of imports of many raw materials has improved compared with November . For example, the two-year compound growth rate of copper ore imports was 3% , up from 1% in November . Changes in the structure of exports in December more reflected a small improvement in global supply chains. Is the change in export structure in December dominated by demand factors or supply factors? We think both may play a role, but the latter may be a little bigger. On the one hand, changes in the structure of overseas demand will not cause a sharp sudden change in one or two months, and the export growth rate of labor-intensive export products in South Korea and Vietnam also generally improved in December . Part of the reason for the decline in the growth rate of China's labor-intensive products may be attributed to the substitution effect on China's labor-intensive product exports brought about by the reduced impact of the epidemic in Southeast Asia. On the other hand, the global supply chain has shown signs of slight improvement recently, with the resumption of work and production in Southeast Asia, the marginal improvement in the delivery time of global manufacturing PMI suppliers, and the slight improvement in global port congestion. The global supply chain bottleneck of high-tech product exports has improved. In December , the two-year compound growth rate of South Korea's semiconductor exports was 33% , higher than the 28% in November , and the two-year compound growth rate of China's integrated circuit imports in December was 27%. , higher than 19% in November , which effectively eased the supply-side constraints on the export of high-tech products represented by mobile phones. At present, the improvement of the global supply chain is still relatively marginal, and China's export freight rates have recently risen again, which may squeeze the export of some labor-intensive products with lower value. Changes in export structure are also reflected in export prices. The year-on-year growth rate of export prices calculated by export value and customs supervision business freight volume increased in December , which is contrary to the intuitive feeling of the decline in the year-on-year growth rate of PPI and the price changes of major export products. We believe that this reflects more changes in the export structure, that is, the increase in the proportion of high-tech products with higher value per unit weight in exports has led to a larger increase in the export price calculated based on the total volume. It is expected that the export price index published by the General Administration of Customs will increase There should not be such a big deviation. The impact of Omicron virus on global supply chain may be smaller than that of Delta virus. On the one hand , the death rate of Omicron virus may be lower than that of Delta virus. On the other hand, the vaccination rate of other export-oriented emerging market economies has increased significantly compared with the impact of Delta virus in August -October 2021. Therefore, we expect other exports In the face of this round of Omicron virus, the strictness of epidemic control in emerging market economies may be lower than when the Delta virus hit in August -October 2021 , and the negative impact on the global supply chain may also be less than at that time.

3. New social financing in December 2021 is lower than expected, and new credit is still weak. The new social financing in December was 2.37 trillion yuan, lower than Winds consensus estimate of 2.43 trillion yuan, an increase of 650 billion yuan year-on-year, mainly driven by the issuance of government bonds: In December , the net financing of government bonds was 1.17 trillion yuan, compared with 2020 . In the same period, it increased by 460 billion yuan. New credit in December was 1.1 trillion yuan, still relatively weak, lower than Wind's consensus forecast of 1.2 trillion yuan, and lower than December 2020 's 1.26 trillion yuan and December 2019 's 1.14 trillion yuan. The year-on- year growth rate of social financing recovered slightly to 10.3 % in December from 10.1% in November .

Interpretation: The structure of increasing credit also needs to be improved, and efforts are still needed to stabilize credit. Specifically: First, banks may extend some medium and long-term loans to January 2022 for a good start , and in December 2021, more bills will be charged. New credit to the real sector was 1.03 trillion yuan in December , of which 40% ( 408.7 billion yuan) was financed by bills, 11 percentage points higher than the same period in 2020 and 38 percentage points higher than the same period in 2019 . And in December 2021 , the interest rate of bills falls below DR007 , and the income of bills may already be lower than the cost of capital, and such impulse may not be sustainable. Second, the improvement momentum of residential mortgage loans has weakened. Since the policy adjustment in October 2021 , the amount of medium- and long-term loans to residents has stabilized. After five consecutive months of negative year-on-year growth, new medium- and long-term loans to residents showed a year-on-year increase in October-November . However , new medium and long-term loans to residents in December were 335.8 billion yuan, down from 439.2 billion yuan in December 2020 and 482.4 billion yuan in December 2019 . In the context of no fundamental improvement in real estate sales, it is difficult for the demand for residential mortgages to recover continuously. The stabilization in the previous two months may be partly related to the release of the backlog of loan applications in the previous period. Third, medium and long-term corporate loans are still weak. In December , new medium and long-term loans to enterprises were 339.3 billion yuan, lower than the 550 billion yuan in the same period in 2020 and 397.8 billion yuan in the same period in 2019. The year- on-year decline in new medium and long-term loans to enterprises continued to remain above 200 billion yuan and has not stabilized. The strengthening of fiscal easing signals is mainly reflected in the accelerated issuance of government bonds and the accelerated placement of fiscal deposits. In December 2021 , the net financing of government bonds was 1.17 trillion yuan, an increase of 460 billion yuan compared with the same period in 2020 ; although the income from bond issuance increased, fiscal deposits in December 2021 fell by 1.03 trillion yuan, a decrease of 9540 yuan in the same period of 2020 . billions have been expanded. In addition, in December 2021 , the net financing of urban investment bonds was 210 billion yuan , which remained above 200 billion yuan for two consecutive months . The average net financing volume of about 50 billion yuan has increased significantly. However, there are a few points to pay attention to: first, although the issuance of urban investment bonds is relatively fast, the supervision of liquidity loans is relatively strict. There is still a certain distance in the amount of land transfer, and it is not ruled out that a small amount of funds may be used to maintain local operations and resolve local hidden debts. Third, the decline in land sales revenue may also restrict fiscal efforts. The increase in the growth rate of money supply is not due to the expansion of bank balance sheets, but is more affected by temporary factors. M2 is the deposits of the non-financial sector, that is, the liabilities of the bank, and its changes come from two aspects, on the one hand, from the expansion of the bank's balance sheet, and on the other hand, from the allocation between different liabilities. Banks create deposits through credit. If this part of deposits is in the hands of residents and enterprises, then M2 will be increased . This is the first aspect we said. If residents or enterprises hand over deposits to the government (tax payment), then M2 decreases; if residents or enterprises purchase financial products, and the financial products allocate this part of the funds to the bonds issued by the bank / additional equity financing, this part of the funds will be reduced. Not counting deposits, it will also reduce M2 . Judging from the changes in the past two years, the accelerated expansion of the balance sheet will bring about an upward trend in the growth rate of M2 , but the impact of the allocation of different debt funds on the growth rate of M2 is more temporary. The year- on - year growth rate of M2 in December increased from 8.5% in November to 9.0% , which is more affected by the distribution of different debt funds, and is likely to be temporary. According to our estimates, the year-on- year growth rate of M2 in December was 0.5 percentage points higher than that in November , of which 0.4 percentage points was contributed by the redistribution of debt funds (excluding fiscal deposits). Looking ahead, further aggregate easing policies in the first quarter are still to be expected. The tone of the Central Economic Work Conference for stabilizing growth has been clarified, and stabilizing credit is an important part of stabilizing growth, which requires both the support of structural monetary policies and adjustments in aggregate policies. At present, the demand for credit in December is still weak, the credit structure needs to be improved, and the year-on-year growth rate of social financing is relatively slow. If the current policy strength is not enough to support the stabilization and recovery of credit growth, and considering that there is still a certain lag from the acceleration of credit supply to the recovery of the economy, the first quarter is still the most suitable window for further easing of monetary policy.

In last Monday's foreign exchange weekly report, we immediately reminded that the US index will weaken in the short-term cycle. At present, the market trend is as I expected, but at the same time, we also mentioned in last week's weekly report that the decline may not be very large. Last week, the US index The lowest fell to around 94.6 , slightly exceeding our expectations; currently, the bottom support is in the range of 94.0-94.4 . At present, the US index has weakened in all cycles except the monthly line, and it is expected to remain weak before the Lunar New Year; the rebound trend of the euro is also more obvious. , and the US dollar is expected to form a resonance; this round of the US dollar adjustment is undoubtedly based on buying, and the medium and long-term trend is not hindered for the time being ( above 6M ). In terms of RMB, affected by the weakening of the US dollar and the settlement of foreign exchange at the end of the year, the RMB once rose above the 6.34 mark on Friday, setting a new high in 42 months. We are still cautiously optimistic about the spot trend of the RMB in the short term. In the long run, since the fourth quarter of last year, we have repeatedly It is recommended that exporters seize the opportunity of higher swaps to lock in the one -year exchange rate. At present, this strategy is also very successful (one-year swaps fell from 1800 to 1200 ). Expected this week RMB 6.30-6.37 .

Market dynamic tracking

Data source: Wind Hong Kong TreasuryMarkets Association HGNH International R&D Center

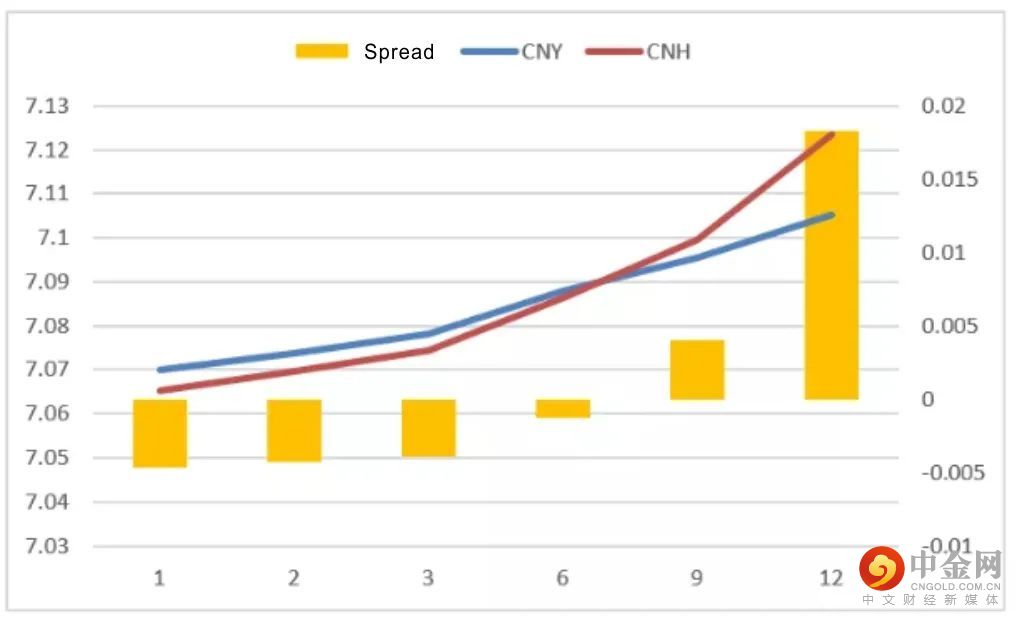

Short-term overseas discounts are domestic,long-term premiums, while the forward price difference between the two placescontinues to narrow.

Data source: Wind HGNH InternationalR&D Center

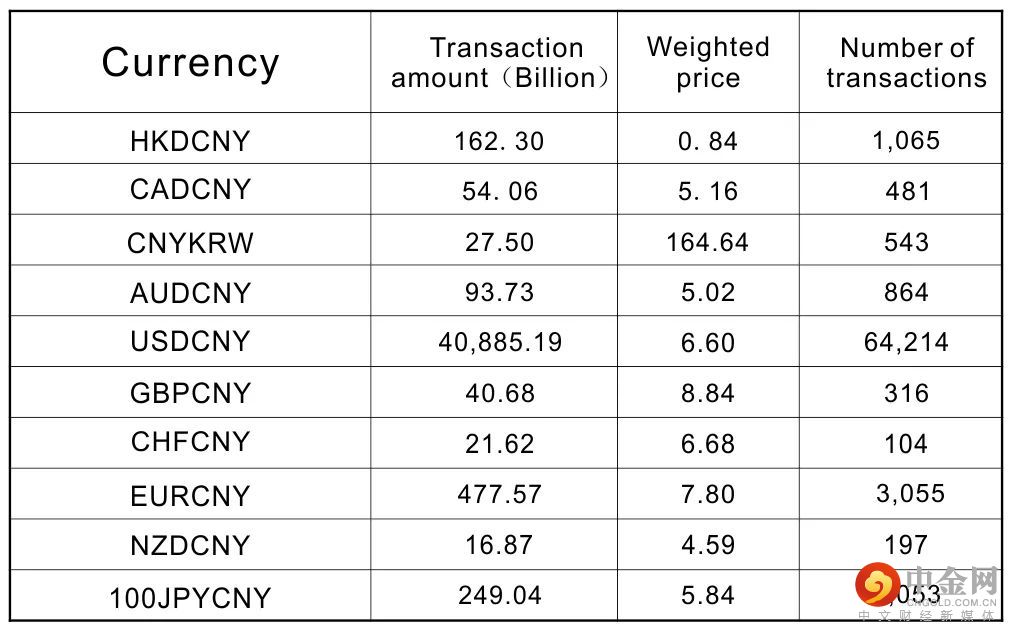

October spot trading volume of importantrenminbi currency pairs

Data source: Wind HGNH InternationalR&D Center

Disclaimer

The information in this report is derived from publicly available information. Although we believe in the reliability of the source of the information in the report, our company does not guarantee the accuracy and completeness of the information. Nor does it guarantee that the opinions and suggestions made by our company will not undergo any changes. Under any circumstances, the information in our company‘s report, the opinions and suggestions expressed, and the data, tools and materials contained in it cannot be used as yours. The absolute basis for futures trading. Since the report was compiled with the analyst’s personal views and opinions and analysis methods, any inconsistencies and different conclusions with other information released by HGNH International will not avoid doubts. The views contained in this report do not represent The position of HGNH International, so please refer to it carefully. Our company does not bear any form of loss caused by futures trading operations conducted in accordance with this report.In addition, the information, opinions and speculations contained in this report only reflect the judgment of HGNH International on the date specified in this report, and can be modified at any time without prior notice. Without the permission of HGNH International, the contents of this report shall not be transmitted, copied or distributed in any way to any other person, or put into commercial use. If you follow the original text for quotation and publication, you must indicate the source “HGNH International” and reserve all rights of our company.

*The above content is translated by Google, the information provided is for reference only and does not constitute any investment advice, and the Company makes no representations or warranties, direct or implied, as to its accuracy or completeness.

举报电话: 13816368049