StraitsFinancial

时瑞金融为CWT集团旗下的金融衍生品服务商,致力于为客户提供差异化和增值服务。公众账号旨在帮助业内朋友增进对海内外金融行业,特别是衍生品领域的了解。欢迎关注、合作、交流与共享。

上海

收录于合集

#首席谈

34个

Issue 242022.12.12

After an abrupt and unexpected reopen in China…

Mr. Hou Zhenhai

Straits Financial (China) Chief Strategist

Review of Last Views:

We expect the Fed's rate hike in December FOMC will slow down to 50bps. In China, driven by the expectation of zero-Covid policy relaxation, as well as a sentiment recovery of A shares and Hong Kong stocks on the previous overly pessimistic expectations, the market rebound will continue. Stock names with a large short-selling ratio in the previous period, esp. Hong Kong index and US listed tech-stocks, will have a relatively large rebound space (25-30% overall). However, due to relative smaller overall decline of A shares, its room for rebound will be relatively small (10~15%). We believe that the overall rebound space of US stocks is more limited.

Main Points:

1. The actual speed of reopen have greatly exceeded our and market expectations. This not only reflects the government's judgment on a low Omicron mortality, but also reflects the increasing urgency to stabilize the economy due to mounting economic pressure and risks.

2. But at least in the next 3 to 6 months, the peak infection period will still have large negative drag on actual economic activities and outdoor consumptions. Therefore, to change the current unfavorable economic situation, China still needs more accommodative macro policies in the future, and we may even see more stimulus and easing policies, so as to help residential sector withstand the peak infection period, as well as improve their income expectations and repair their balance sheets.

3. The rebound in overseas markets in the past one and a half months was mainly driven by the fact that ON RRP on the Feds balance sheet dropped by US$400 billion through FOMO. However, with the improvement of liquidity and risk appetite, this may has ended, which may mean that the improvement of risk appetite in overseas markets is also coming to an end.

4. Under the current high interest rate level, even if the Fed lowers its rate hike to 50bps, it will still have a significant tightening effect on the economy and market liquidity. However, as the US job market is still stable and the growth rate of labor wages has rebounded in November, which means that the Fed lacks fundamental reason for a shift in its monetary policy stance.

5. The domestic market continues to be in an environment of “positive expectations vs weak economy”, although optimistic sentiment on reopen has been reflected in A-shares and Hong Kong stocks. In the future, the market's focus will gradually shift to possible domestic macro stimulus policies. Investors need to pay close attention to the Central Economic Work Conference to be held in mid-December, which may provide more color on future possible stimulus policies. If there are large scale stimulus coming out, A shares and Hong Kong stocks may continue to rally.

6. As for the overseas stock market, we believe that the short-term rebound is coming to an end. It is expected that the market sentiment indicator, which is currently at the highest level this year, will fall again and lead to a correction in overseas risk asset prices. We are relatively neutral on commodities. On the one hand, some commodities may continue to benefit from the optimistic sentiment of Chinas reopen and potential incoming stimulus. On the other hand, the short-term US dollar index may gradually stabilize or even rebound slightly. This may put some downward pressure on the prices of some commodities.

I

In last month's report, we suggested that China's zero-Covid policy may be marginally relaxed, but the actual speed of reopen have greatly exceeded our and market expectations. We believe that the main reason for the beyond-expectation loosening of zero-Covid control is firstly that the current Covid outbreak areas in China, such as Guangzhou, Chongqing and Beijing, have a very low overall severity and mortality rate; secondly, the domestic economy has recently experienced a severe slowdown, due to the previous strict zero-Covid closedown. Based on the judgment of the above two points, we believe that as long as there is no serious large-scale unexpected death after open-up in China (at present, unless there are new and more toxic mutations in Omicron, this probability is very low), and domestic Covid related restriction will continue to relax until it is completely released.

Of course, from the perspective of the Covid itself, since the current number of infection is still very low in China, the large-scale infection outbreak across the country in the future will be basically a certain event. In particular, the next two months will coincide with the New Year's Day and Spring Festival holidays, and the sharp increase in holiday travelling may lead to a rapid increase in nationwide infections. Therefore, for at least 3 to 6 months, Covid will still have a relatively large negative drag on actual economic activities and outdoor consumption. Because during this period, there will always be some people who will temporarily leave their jobs and outdoor activities due to infection, and more importantly, peoples worries about infection, especially for middle and elder ages and people with underlying diseases, will cause their outdoor activities and willingness to spend in a decline. If during that period, China can maintain the normal status of medical service sector, et. there is no shortage of medical resources due to the large-scale infection of medical staffs, we believe that this concern may gradually subside after 3 months, but if there is a shortage of medical resources, the overall social anxiety could last longer.

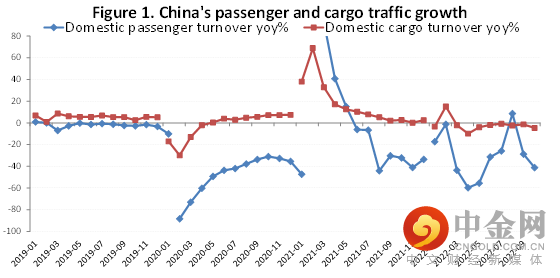

Therefore, we believe that the current relaxation or even cancellation of Covid restriction is not enough to change the downward pressure on the economy. To achieve that, China still needs more accommodative domestic macro policies in the future, and we are likely to see the introduction of more stimulus and easing. For example, the current domestic passenger turnover still fell by 40% year-on-year, and the cargo turnover fell by 5% year-on-year (Figure 1).

Source: Bloomberg, CEIC, Wind

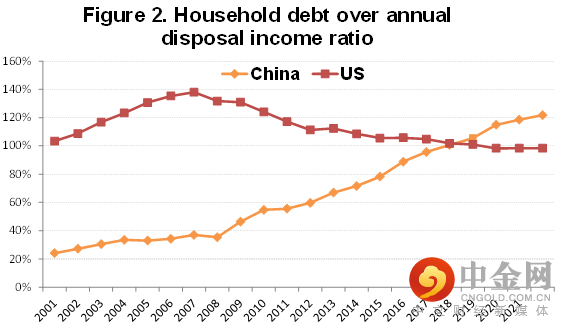

If there is just a reopening but without further stimulus, we believe that 1H2023, these two indicators can only rebound to around -15% and 5%, that is to say, it is still not enough to guarantee China's GDP growth next year to reach about 4~5%. In comparison, the main reason behind the strong consumption turnaround in EU and the US after their reopening is that they generally adopted aggressive fiscal and monetary stimulus during the pandemic period, including direct large-scale cash subsidies to the households, etc. As a result, the overall income of residents in the US were actually in a steady growth instead of decline in the past three years. However, during the three-year period of Covid in China, the fiscal stimulus has provided very limited help to the household sector. Therefore, the income growth rate of the Chinese residential sector has shown a continuous slowdown, and the debt repayment pressure has continued to rise (Figure 2). Therefore, further fiscal and monetary policies to help households to withstand the incoming peak infection period, while improving future income growth expectations and repairing household balance sheets are an important variable for China's economy to get out of the impact of the Covid next year and return to its potential growth.

From the perspective of the financial market, it is still generally in a state of “positive expectations vs weak economy”. On the one hand, the short-term negative impact of Covid and the drop in exports will further cause downward pressure on the economy, but the market expects that after the end of closedown and a rapid peaking infection, the country will usher in a significant economic growth and a rebound in corporate profits. It's just that the market is still divided on whether this rebound will appear in Q2 of next year or in 2nd half of the year. In our view, positive expectations are more beneficial for the stock market, because the stock market as a whole tends to trade more based on expectations than reality. Therefore, we maintain a neutral-to-bullish view on the domestic stock market. As long as the Covid mortality rate does not deteriorate significantly and the reopening policy tends to remain unchanged, the domestic stock market has limited downside risks in the near future. The opportunity for further rise in the domestic stock market mainly comes from potential future macro stimulus policies. Therefore, investors can first pay attention to the upcoming Central Economic Work Conference to be held in mid-December, when policymakers may specify more policy measures to ensure the stabilization and recovery of the economy in 2023.

II. Overseas markets‘ rebound based on improving liquidities and easing expectations on Fed’s rate hikes may end soon.

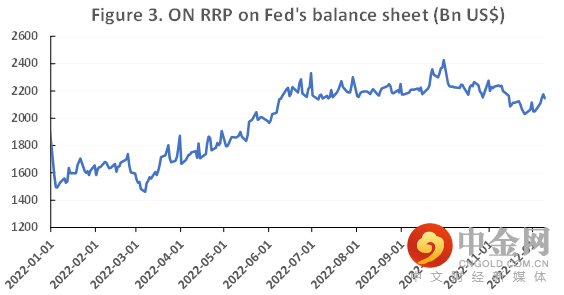

Overseas markets have also experienced a relatively significant rebound since mid-October, during which the US stock index and commodity prices rallied, bond yields and the US dollar index fell. All these were generally reflected in a significant rebound in market risk appetite. We believe that the rebound in overseas markets in the past one and a half months is mainly driven by the fact that the ON RRP on the Fed‘s balance has dropped by nearly US$400billion. As a result, the ON RRP which were at its highest in early October around US$2.42 trillion fell to US$2.03 trillion on November 25 (Figure 3). The reason behind this FOMO changes, as we believe, is mainly due to a market’s selloff in September on tighter liquidity and some event factors, such as the turmoil in the UK financial market and a worry of EU energy shortage, which resulted in a market panic and trading on potential crisis risks.

Source: Bloomberg, CEIC, Wind

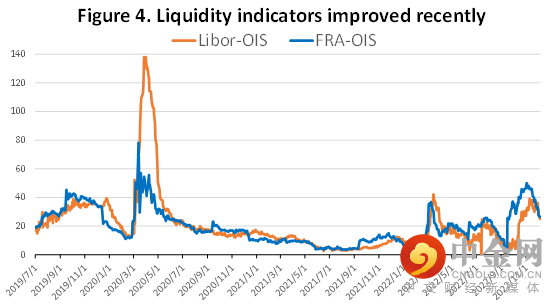

However, with Feds FOMO and worry of systematic risks gradually subsiding, the current market liquidities and expectations have been greatly improved. For example, compared with October, major liquidity indicators such as Libor and FRA spread have dropped significantly (Figure 4). Therefore, in the current environment, the need for the Fed to further inject more liquidity into the market is rapidly decreasing. So we can see that starting from December, the Fed no longer continues to inject more liquidity into the market through FOMO. At the same time, the Fed's QT continues, at its maximum pace of US$95 billion per month. If the Fed maintains its current operation, the marginal improvement in market liquidity will come to an end, and liquidity will tighten gradually again in the future, leading to the end of this round of rebound in overseas markets based on improved liquidity and risk appetite. Of course, we believe that the Fed will still can use its ON RRP as a liquidity buffer when there is liquidity tightening in the market in the future or when the economic fundamentals worsen again. But the whole picture is still to gradually and steadily tighten to control inflation and strive to achieve a soft landing of the US economy. But it is obviously unlikely that the Fed will stop monetary tightening under the current inflation and economic conditions.

Source: Bloomberg, CEIC, Wind

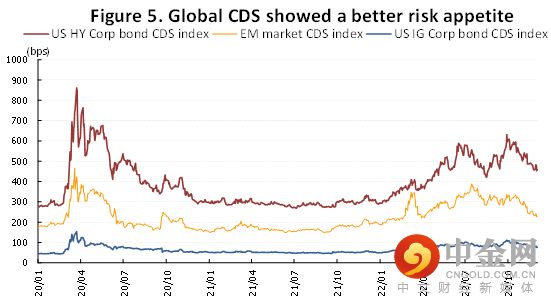

At the same time, we see that the increase in risk appetite is universal in this round. On the one hand, it is across all asset classes, i.e., it has an important impact on stocks, bonds, commodities and foreign exchange rates. At the same time, it is also cross-regional, so it is not only US stocks and bonds, but also affects global asset prices. Credit spreads have shrunk significantly, not only the CDS of corporate bonds in Europe and the US, but also in EM markets (Figure 5). That is to say, the current overseas market is a macro driven market, and more specific speaking, a market almost entirely driven by the Fed's policy actions, as a result, the correlation between various asset trends is still very high.

Source: Bloomberg, CEIC, Wind

III.

US economic fundamentals determines that Fed will not change its course soon

In last month‘s report, we said that the Fed will reduce its rate hike to 50bps starting from December FOMC, and this has now basically been confirmed by the Fed. But we don't think this means that the Fed's monetary policy attitude has changed. First of all, with the current federal benchmark policy rate at 3.75~4%, the necessity of 75bps hike has obviously been reduced, but even with a 50bps hike each time, considering the current rate is already very high, it will still have more significant tightening effect on the economy and market liquidity. At the same time, after the Fed’s 50bps hike in December, there is still uncertainty about whether the Fed will further lower its hike to 25 bps at the next FOMC in early February next year.

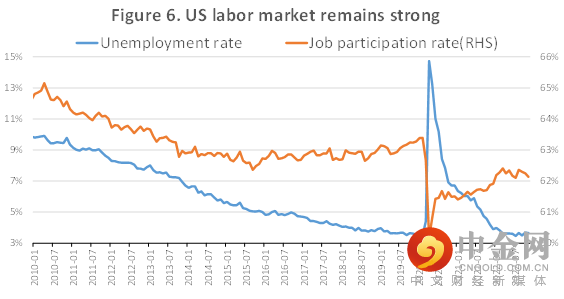

Judging from the recently released US economic data, however, the US job market remains relatively strong, with the unemployment rate still at a historically low level, and the employment participation rate even falling for several months in a row (Figure 6).

Source: Bloomberg, CEIC, Wind

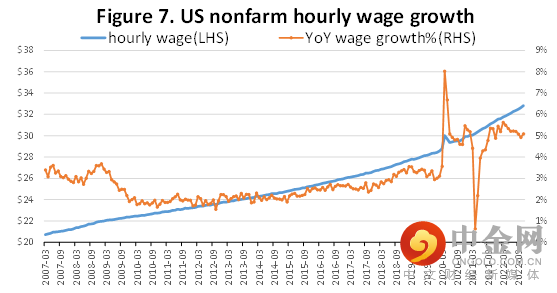

At the same time, the US nonfarm hourly wages in November increased by 0.7% MoM, and the YoY growth rate rebounded from 4.73% in October to 5.09% in November (Figure 7), which reflects that the overall wage inflation environment in the US has not improved recently. This indicates that the overall inflation environment in the US still does not provide a condition for the Fed to make a quick policy turnaround for a period of time to come. Therefore, on the premise that there is no significant systemic risk in the overall US economy and financial market, while the job market is still tight, and the inflation level is still difficult to fall back to the range acceptable to the Fed in the short term, we believe that it is very difficult to expect the Fed to turn around prematurely.

Source: Bloomberg, CEIC, Wind

IV. Market strategy

Chinas reopen has significantly improved investors' expectations, but this has mostly been reflected in the current A shares and Hong Kong stock market sentiments. In the future, the market's focus will gradually shift to possible domestic macro stimulus policies, and investors would evaluate whether the strength of these policies can help the economy overcome the economic pressure due to peak infection period in the first half of next year and the decline in external demand and exports. In general, the stock market may benefit more from optimistic expectations. Therefore, we believe that A shares and Hong Kong stocks still have a certain rebound space, while the downside risks are limited. Investors need to pay close attention to the Central Economic Work Conference to be held in mid-December, which may provide more color on future possible stimulus policies. If there are large scale stimulus coming out, A shares and Hong Kong stocks may continue to rally.

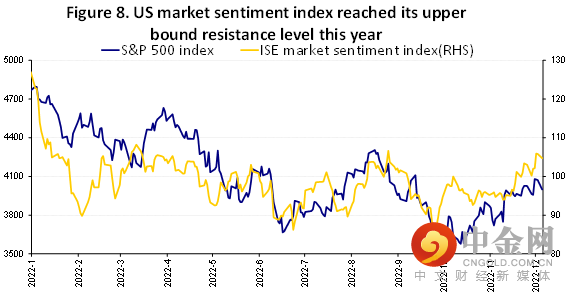

As for the overseas stock market, we believe that the short-term rebound is coming to an end. As the ON RRP on Feds balance sheet stabilizes, it is hard to maintain the US stock market sentiment indicators, which had reached its resistance upper bound level this year (Figure 8). It is expected that market sentiment will fall again and lead to a correction in overseas risk asset prices.

Source: Bloomberg, CEIC, Wind

We are relatively neutral on commodities. On the one hand, some commodities may continue to benefit from the optimistic sentiment of Chinas reopen and potential incoming stimulus. On the other hand, the short-term US dollar index may gradually stabilize or even rebound slightly. This may put some downward pressure on the prices of some commodities.

免责声明:本文件仅供参考。本文件并非作为或在任何情况下被视为对任何资本市场产品的招揽;或购买或出售的要约或要约意图。本文件的内容也不构成对任何人的任何资本市场产品的投资建议。本文件所包含的所有信息均以公开资料为依据,所载资料的来源及观点的出处皆被时瑞金融在发布本文件时认为准确和可靠,但时瑞金融不能保证其准确性或完整性。时瑞金融不对因任何遗漏,错误,不准确,不完整或其他原因而遭受的任何损失或损害(不论是直接,间接或后果性损失或任何其他经济损失)承担任何责任。期货合约、衍生品合约与商品以往的表现或历史数据并不代表未来表现,不应作为日后表现的依据或担保。时瑞金融有权在不通知的情况下随时更改本文件的信息。

#首席谈

34个

下一篇

【时瑞金融首席谈】超预期疫情管控开放之后

举报电话: 13816368049