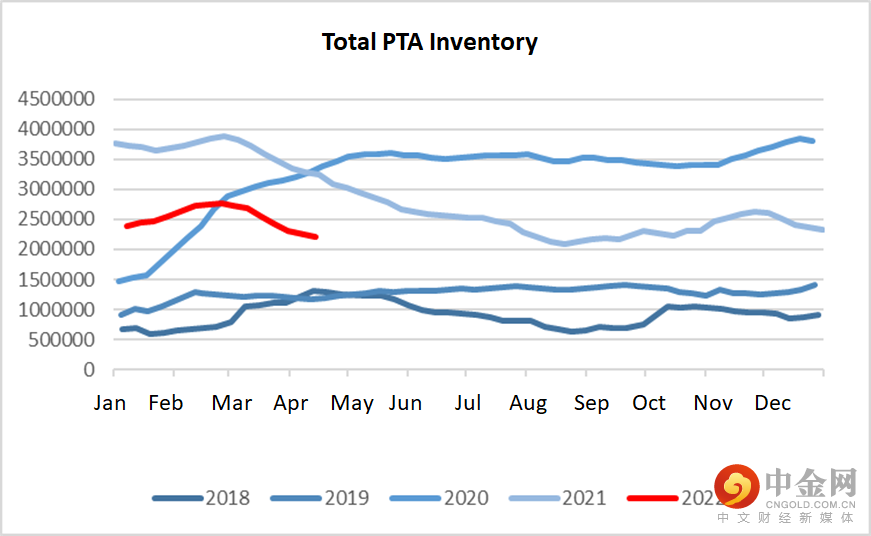

The price of PTA futures has continued tofluctuate and rise since December. This trend has followed the price of crudeoil, mainly due to the strong supply and demand of PTA. The expectation in thefutures market is stronger than the spot market, and there is a seasonalaccumulation of stocks from January to February and destocking from March toMay.

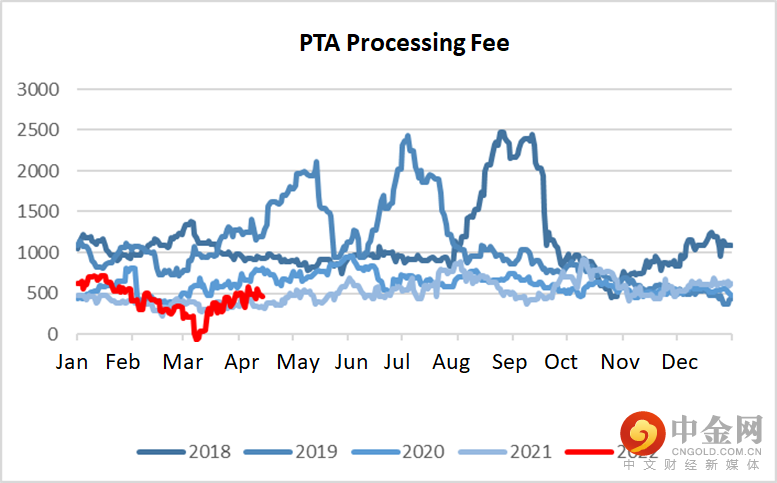

The average processing fee of PTA last yearwas 500 yuan/ton. In March, the processing fee on the spot market was in therange of 200-300 yuan/ton, which was at the lowest position in history. Withthe overhaul of Yisheng Petrochemical, the operating rate of TA will be reducedto less than 70%. Under the pessimistic demand expectation, it is still in thestate of destocking and the overall pattern is strong. There is still potentialfor increasing processing fees in the later stage when demand improves.

The following PTA plants have recently beenshut down for maintenance:

1. Honggang Petrochemical's 1.5 mnt/yr plant was shut down on March 15, restarting date to be determined;

2. Fuhua cut the operating rate ofits 4.5 mn t/yr plant to 50% in early April;

3. Yadong Petrochemical's750,000-ton plant was shut down on April 6th;

4. Sinopec Yangzi shut its 1.2 mn t/yr planton March 14thand plans to resume production in mid-May;

5. Yisheng New Materials shut downPTA Production Line 1 at the end of April; Yisheng Dalian shut down PTAProduction Line 2 in mid-May; Yisheng Hainan shut down the PTA plant in lateMay;

6. Hengli Petrochemical shut down250 mn t/yr unit on March 10th for 10 days maintenance and 220 mn t/yr unit for20 days maintenance from April 10th;

7. The 1 million-ton plant ofSichuan Energy shut down a 1mn t/yr plant in mid-April;

8. Zhongtai Chemical shut down a 1.2t/yr plant at the end of March.

There is a long-term shut down formaintenance in the following PTA plants:

1. Sinopec Yangzi shut down350,000 tons plant on December 3rd 2020, restart date to be determined;

2. Huabin Petrochemical shut downa 1.4 mn t/yr plant on March 3rd 2021, restart date to be determined;

3. Liwan Polyester shut down aplant with capacity of 700,000 t/yr on March 6th 2021;

4. Sinopec Shanghai shut down aplant with capacity of 400,000 t/yr on February 20th 2021;

5. Tianjin Petrochemical shut downa plant with capacity of 340,000 t/yr in April 2020;

6. PetroChina Urumqi shut downplant with capacity for 75,000 t/yr in April 2021;

7. Hanbang Petrochemical shut downa plant with capacity of 700,000 t/yr in May 2020 and 2.2 mn t/yr plant onJanuary 7th 2021;

8. Pengwei Chemical shut down aplant with capacity of 900,000 t/yr in March 2020.

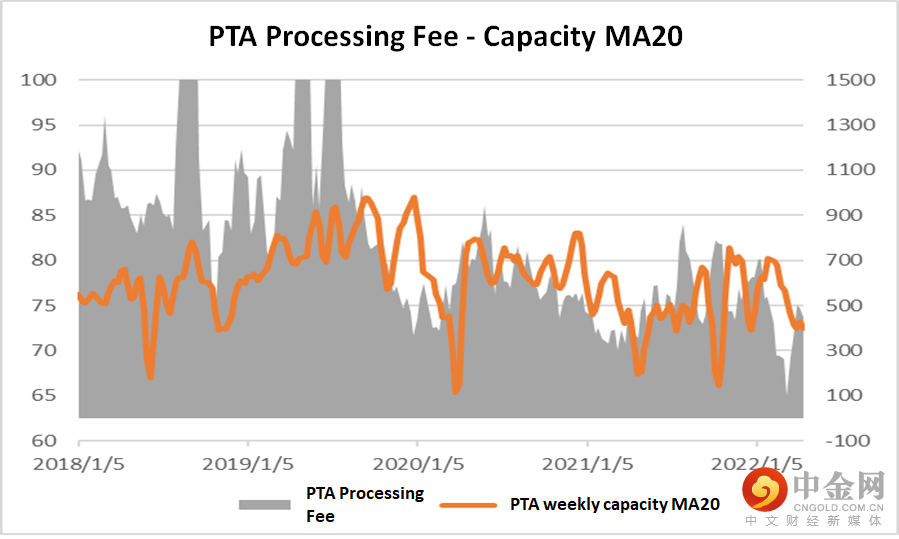

From the profit distribution of crude oil,Naphtha, PX and PTA, it can be seen that profits are mainly concentrated in therefined oil part, and profit margins for downstream industrial products aresqueezed. PXN and PTA processing fees are at the lowest point in history. Byfitting the processing fee and operating rate of PX-PTA, we can see these twofactors have high goodness of fit. The production plants react to squeezedprocessing fees by initiating shut down maintenance in advance or delayingproduction resume date, to stimulate PTAs price and bring processing fee backto a normal level. It is widely acknowledged that the PTA industry is doingwell, the low processing fee is not reasonable given the current decreasinginventories and growing exporting situation. It is expected that the processingfee in the second quarter will be in the range of 500-1000, and the absoluteprice of PTA will increase with that of crude oil.

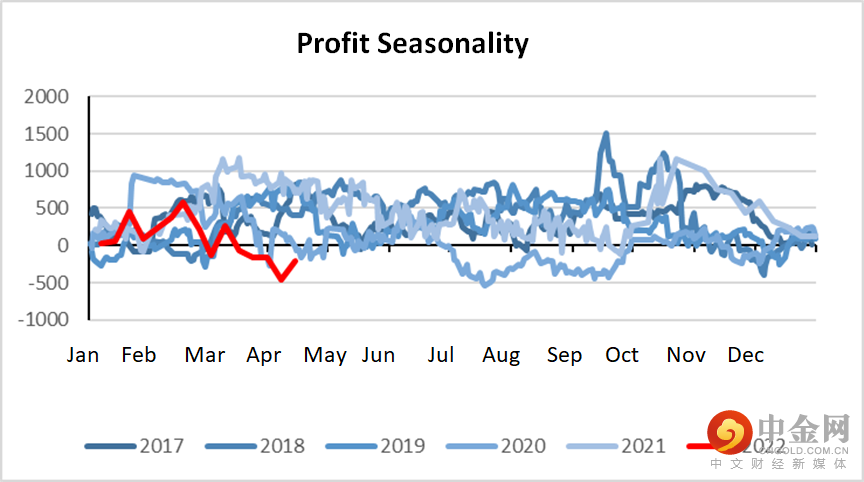

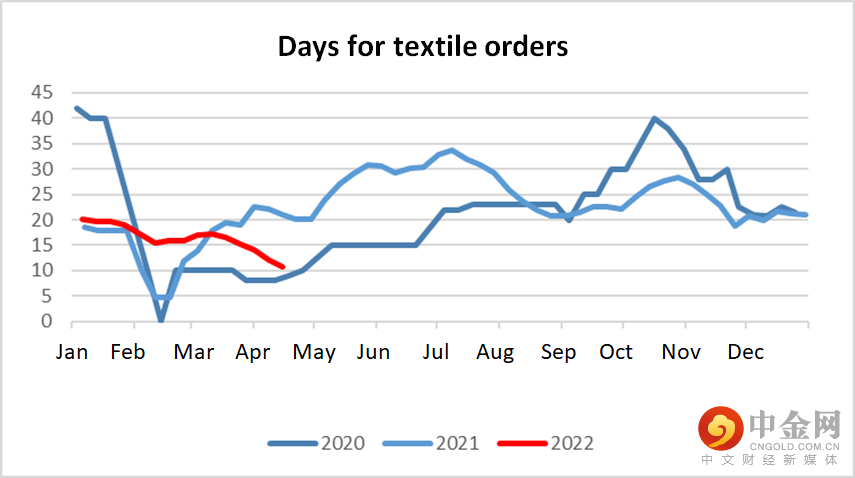

The current demand is weak due to thecovid-19. On the one hand, the covid-19 situation suppresses the textile demandand reduces the efficiency of the supply chain. Recently, the cost side hasgradually recovered strongly, the epidemic continues to suppress the price,price of polyester lacks upward momentum. The turning point has gradually shownsigns, the interest rate cut has landed, the policy support has been exerted inadvance, and the strong expectation corresponding to the pessimism of realityhas gradually begun to reflect the value of the transaction. On the other hand,the suspended production due to the epidemic has begun to resume at a fastspeed because of the more precise and efficient epidemic prevention policy.

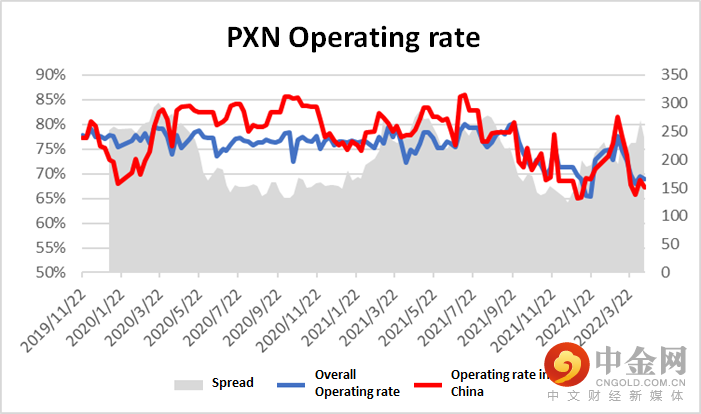

The opportunity for polyester is in crudeoil and on the demand side. Currently, crude oil price remains high, PXN priceis at $240, PTA processing fee remains $ at 500, and there is profit inNaphtha- TA part. Although the production capacity of polyester has decreased,there has not seen much reduction in the demand. The downstream has started toraise production capacity recently, it can be expected that the productioncapacity of polyester would soon rise in half a month. However, thecorresponding supply sides of PX and TA are experiencing shutdown maintenanceon a larger scale and longer time, which reduces the supply. In the short term,the price of TA would follow the crude oil price with a wide fluctuation. Inthe medium to long term, 09 has a stronger upward momentum.

Disclaimer

The information in this report is derived from publicly available information. Although we believe in the reliability of the source of the information in the report, our company does not guarantee the accuracy and completeness of the information. Nor does it guarantee that the opinions and suggestions made by our company will not undergo any changes. In any case, the information in our company‘s report, the opinions and suggestions expressed, and the data, tools and materials contained in it cannot be used as yours. The absolute basis for futures trading. Since the report was compiled with the analyst’s personal views and opinions and analysis methods, any inconsistencies and different conclusions with other information released by Nanhua Futures Co., Ltd. will not avoid doubts. The views contained in this report are not It represents the position of Nanhua Futures Co., Ltd., so please refer to it carefully. Our company does not bear any form of loss caused by futures trading operations conducted in accordance with this report.

In addition, the information, opinions and speculations contained in this report only reflect the judgment of Nanhua Futures Co., Ltd. on the date specified in this report, and can be modified at any time without prior notice. Without the permission of Nanhua Futures Co., Ltd., the contents of this report shall not be transmitted, copied or distributed in any paradigm to any other person, or put into commercial use. If you follow the original text for quotation and publication, you must indicate the source “Nanhua Futures Co., Ltd.” and reserve all rights of our company.

举报电话: 13816368049